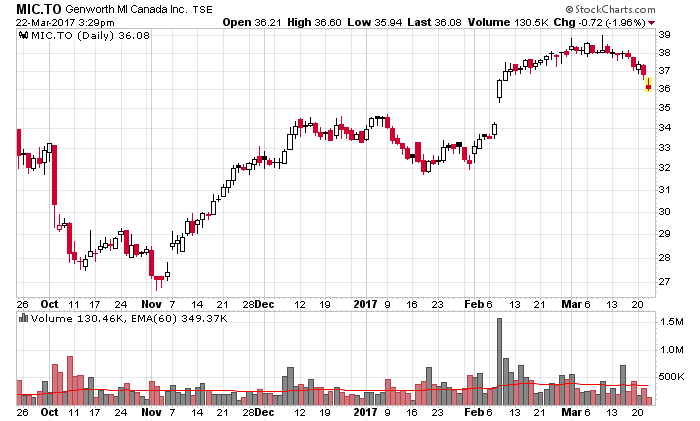

On April 13, three notable companies associated with Canadian housing pricing fell considerably: HCG, EQB and MIC.

There were a bunch of other companies that had issues, but it looks like that the trio above were fairly pronounced in the day’s list of losers:

April 13, 2017 TSX Percentage Losers

| Company | Symbol | Volume | Close | % Change |

| Nthn Dynasty Minerals Ltd | NDM | 4,841,027 | 2.17 | -10.3 |

| Intl Road Dynamics Inc | IRD | 203,203 | 2.81 | -10.2 |

| China Gold Intl Res Corp | CGG | 1,269,594 | 2.43 | -9.3 |

| Home Capital Group Inc | HCG | 972,606 | 21.70 | -8.6 |

| Aphria Inc | APH | 6,005,793 | 7.21 | -8.3 |

| Equitable Group Inc | EQB | 287,512 | 63.41 | -8.3 |

| Fennec Phrmctcls Inc | FRX | 12,537 | 5.50 | -8.0 |

| Silvercorp Metals Inc | SVM | 1,516,993 | 4.94 | -8.0 |

| Alacer Gold Corp | ASR | 1,881,209 | 2.52 | -7.7 |

| Street Capital Group Inc | SCB | 28,489 | 1.40 | -6.7 |

| Taseko Mines Ltd | TKO | 794,675 | 1.52 | -6.2 |

| Trilogy Energy Corp | TET | 182,481 | 4.95 | -6.1 |

| Genworth MI Canada Inc | MIC | 221,174 | 34.63 | -6.0 |

| Top 10 Split Trust | TXT.UN | 9,863 | 4.08 | -6.0 |

| Guyana Goldfields Inc | GUY | 916,012 | 7.41 | -5.4 |

| Golden Star Resources Ltd | GSC | 548,268 | 1.09 | -5.2 |

| Continental Gold Inc | CNL | 852,825 | 3.91 | -5.1 |

| Arizona Mining Inc | AZ | 501,450 | 1.96 | -4.9 |

| Great Panther Silver Ltd | GPR | 387,165 | 2.00 | -4.8 |

| Argonaut Gold Inc | AR | 1,036,644 | 2.43 | -4.7 |

I’ve been trying to find what caused this spontaneous meltdown in equity prices.

My 2nd best explanation is that Bank of Canada Governor Stephen Poloz is putting a torpedo to the Toronto housing market by making explicit statements about the 30% year-to-year rise in valuations and about how there is no explanation for it. Specifically, he stated “There’s no fundamental story that we could tell to justify that kind of inflation rate in housing prices, and so it’s that gap between what fundamentals could manage to explain and what’s actually happening which suggests that there is a growing role for speculation“, which is a mild way of saying that people are basically trading houses in Toronto like they did with Tulip Bulbs in the Netherlands in 1636.

He also politely stated that if you believe that housing prices are going up 20% year-to-year, it doesn’t matter whether he raises interest rates by a quarter or half point, and he could even raise them 5% and it wouldn’t make a difference (although it would be rather fun to see him try and see all the mathematical financial models predicated on stability go out the window in one massive flash crash).

However, my primary reason why I think the three stocks crashed is a simple announcement:

==========================

Media Advisory

From Department of Finance Canada

April 13, 2017

Minister of Finance Bill Morneau will hold a meeting with Ontario Finance Minister Charles Sousa and Toronto Mayor John Tory to discuss the housing market in the Greater Toronto Area.

A media availability will follow the meeting at approximately 3:30 p.m.

Date and Time

2:30 p.m. (local time)

Tuesday, April 18

Location

Artscape Wychwood Barns

601 Christie Street

Toronto, Ontario

==========================

Being somewhat experienced with the nature of government communications, there is no way you can get a federal and provincial Liberal with a Conservative mayor doing a joint announcement on something without it leaking to the marketplace.

The only question here is how deep they’re going to stick their silver-tipped oak stake into the heart of the Toronto real estate vampire.