Almost two months ago (December 7, 2022) we had the key paragraph:

Looking ahead, Governing Council will be considering whether the policy interest rate needs to rise further to bring supply and demand back into balance and return inflation to target.

Now, the forward guidance has been shaded to:

If economic developments evolve broadly in line with the MPR [monetary policy report] outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases.

This is being interpreted as a “If things are in expectations, interest rates will hold steady.”

That said, this quarter point raise is relatively a consensus decision and one that I was expecting myself.

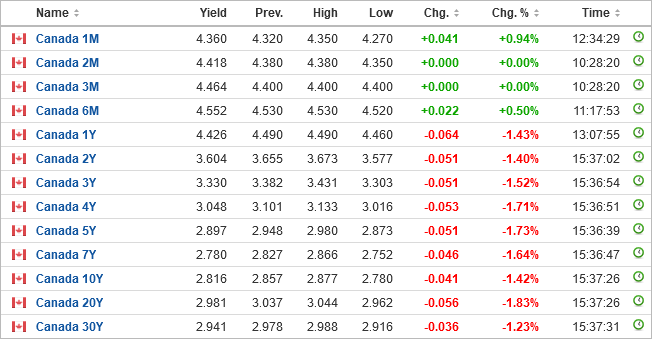

However, the yield curve says otherwise:

The bond market, and also the short-term interest rate futures market, are projecting a rate drop – March 2024 futures have a 3-month bankers’ acceptance rate of 3.65% (right now that 3 month rate is 4.86%).

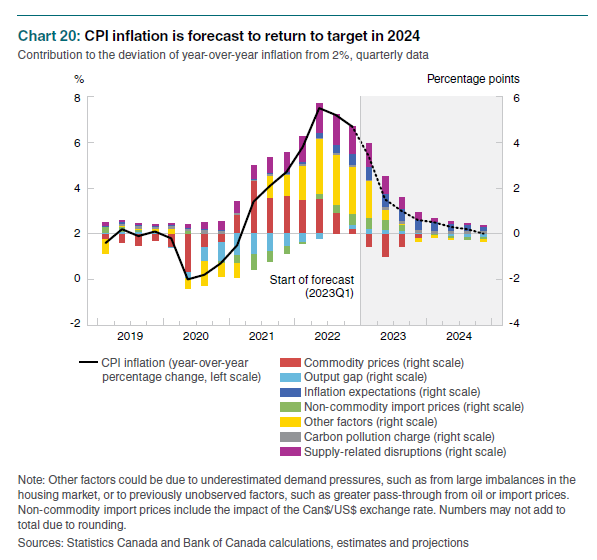

When reading the MPR, we have the following projection of inflation:

Pay attention to the dual y-axis on the chart, specifically where the 2% inflation target lies in relation to various inflation components.

The other item is the huge amount of the yellow component “Other factors”, which is a huge fudge factor that is given little bearing in forward inflation forecasting.

My reading of the tea leaves is that the future is not going to be nearly as easy as presented. My crystal ball is starting to clear up somewhat.

I’m expecting, due to the mathematical quirk of how headline inflation is calculated (year-over-year) that comparisons between March and July will be very favourable. The reason is due to this chart:

Due to the Russia-Ukraine conflict and all of the spillover effects thereof, the baseline energy inputs (which drive a good chunk of industry) will be dissipating.

The change in natural gas pricing is even more drastic. (It is too depressing to post here).

Inflation will obviously be seen as tapering. The markets will declare victory, and there will be a massive push of capital into the equity markets since clearly central banks are done – why get 4-5% on long-term investment grade corporate debt when clearly there’s more opportunity with equities? All of that cash that is on the sidelines will plough in, Gamestop and AMC will have another hurrah, and everybody will have this sense of comfort that Covid is behind us, the damage done in 2021-2022 is over and we can look forward to living happily ever after?

Between now and around the month of May, I would say “risk on”. Recession? What recession? Rising interest rates? No more! Inflation? Dropping!

Where things are going to get really dicey is the time period after September, where it will become really clear what’s going to happen in terms of the conflict and the global trade situation, especially with India and China. The import of materials from China historically was deflationary but things are changing with on-shoring.

We look at the various components of Canadian CPI (Table 1 on this link – scroll to the bottom):

Food (16%) – whether from a store (transportation, F/X, labour) or especially a restaurant (labour, municipal land taxes, and retail REITs passing on higher interest costs to customers), this will increase and I do not see supply conditions improving to mitigate this

Shelter (30%) – especially rents in urban centers (7%), mortgage costs (3%), or raw construction (6%), there is not enough supply, and when you keep cramming in half a million people into the country each year, with no real expansion of supply, the net result here is obvious

Household operations, furnishings and equipment (15%) – This should actually be roughly level.

Clothing and footwear (4.5%) – Steady

Transportation (16%) – A function of energy prices. The car market should stabilize somewhat, you are already seeing used car indexes in the USA begin to flatten, and one-time windfalls on used vehicles are no longer to be had

Health and personal care (5%) – This is a service sector and rates will continue to rise with labour costs

Recreation, education and reading (10%) – Post-covid, there is much continued demand for this and limited supply (e.g. take a look at international flight pricing, and hotel pricing) – this is heading up. There is a huge labour cost component here.

Alcoholic beverages, tobacco products and recreational cannabis (5%) – Up, namely due to taxes and raw input costs.

In general, I see the supply side continuing to have a great impact on pricing – not enough supply is being thrown into the economy.

Think of it this way – when you have central banks saying “We are trying to kill demand by raising interest rates until people feel pain”, are you, as a business owner, going to be putting in long term capital investments into anything consumer-related? No way, unless if you have some sort of secured demand (e.g. government funding – look at how much money the Government of Canada is blowing on EV subsidies at the moment).

Right now, the crystal ball says that inflation will appear to flatten for the first half of the year, but the assumption of the downward trajectory is going to be mistaken.

I suspect the short-term interest rate will remain steady for longer than people expect. Right now the Bankers’ Acceptance futures for September 2023 give a 4.69% expectation – roughly half-pricing in that the Bank of Canada will start to drop rates on their September 6th interest rate announcement.

In the meantime, the true deflationary headwind is still ever present – in the form of quantitative tightening.

These balancing factors (suppressed demand due to high interest rates, limitation of supply from both material and labour and decreased productivity, and monetary compression due to QT) will continue to cause confusion. The strategy of the Bank of Canada is that these factors will balance out. I don’t think they have much choice.

However, later this year, if for whatever reason you see inflation refusing to taper below the 4% point, this really puts the central bank into a quandry. Just beware of future guidance.