In the short term, the market is designed to confuse everybody, but understanding the nature of the confusion is paramount.

Apparently in the past couple days, people have been worried “things will last longer than expected”. I have seen a bunch of stocks get dumped indiscriminately, sort of like a second wave of COVID-19 hitting the financial markets. I’m sure some of you have “felt” this mini-tremor as well. Nervous individuals that have bought shares a week ago are underwater, and are reading these headlines and are starting to panic.

This creates volatility and another round of panicked people want to reach for cash.

The problem is that any time you see a trade on the market, the cash gets exchanged from the person willing to buy the stock to the person that wants to dump the stock. The amount of cash remains the same, just that the valuation of the asset (a residual economic slice of the company in question) changes.

Maybe these people reaching for cash are satisfied with it staying around, effectively taking the cash out of circulation of the economy.

But central banks can wave a magical wand, and exchange bonds for more cash. This cash increases the pressure for demands on assets, which mostly makes its way to the stock market since this is the only game in town where you can get an income. Other routes include real estate (which doesn’t make as much income any more since rents are collapsing as we speak), or commodities (which should retain their value, and in some cases even increase in value depending on their demand). Relatively speaking, the cash becomes less significant with increased liquidity in the marketplace.

So in the medium term, this liquidity getting injected into the financial system will dampen volatility. In the short term there are going to be gyrations in accordance to the changes of participants’ psychologies, which is very rapid as the market tries to price in exactly what will be happening as a result of the COVID-19 reaction.

The cliche is that you need to sell when most participants are too bullish (there’s no incremental demand to convert cash to assets at a price higher than the assets), while the converse is true when more people are too bearish. When everybody wants cash at the same time (like during the third week in March) the result is a crash in asset prices and a huge rise in volatility. The difficult part of timing the bottom is that you have no idea when the last person (institution, pension fund, hedge fund, or a brokerage executing a margin liquidation on a poor client) that absolutely wants to convert the last of their asset into cash at any price he/she can get. You just don’t know, which is why you average when things get a little silly.

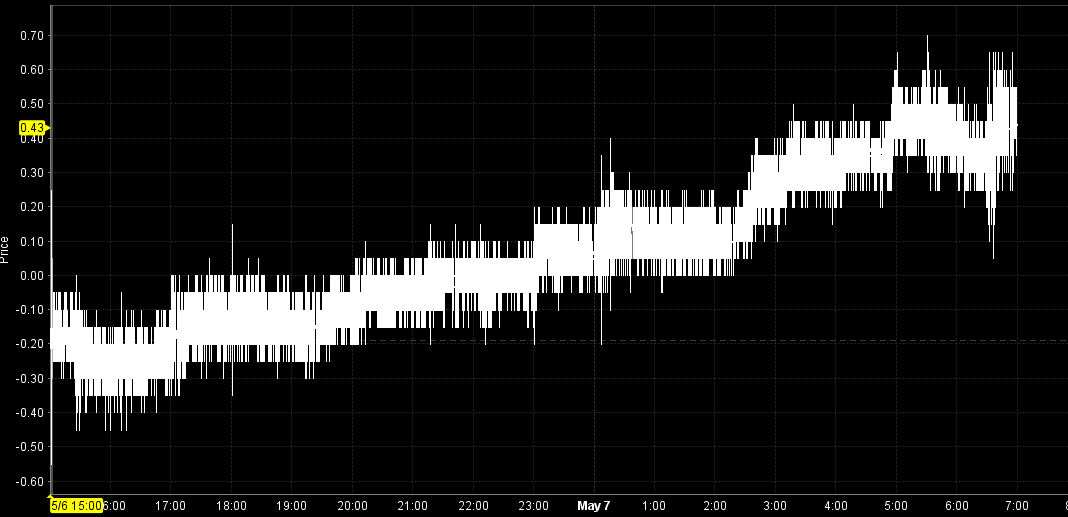

I wrote earlier sometimes it is better to be lucky than good, but yesterday evening I placed some volatility orders and they were reasonably well timed to correspond with the peak of this mini-earthquake we’ve had over the past few days (which was also instigated by the upcoming Friday being an options expiration Friday, which tends to increase volatility).

The risk-reward dynamic of the market is that if a trade feels good, it probably is a sentiment shared with others in the marketplace, and hence it is less likely to succeed than if you were very worried going into a position. And believe me, shorting VIX looks easy in retrospect but it takes nerves when you see the stock chart rocket up.