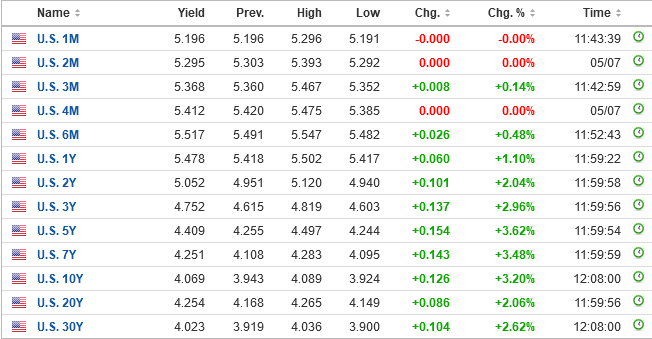

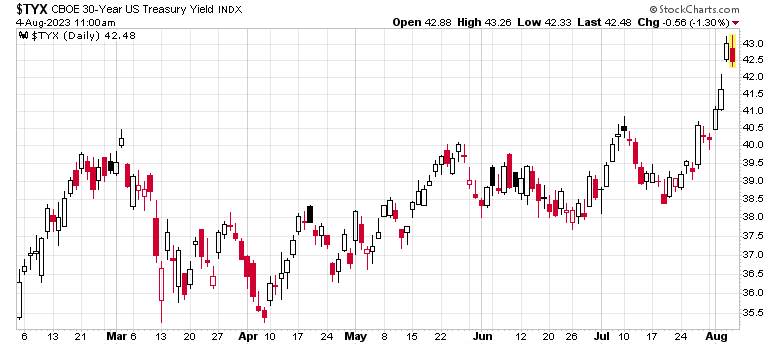

Bill Ackman has made the news about being short 30-year treasury bonds (buying puts on treasuries). You can play this trade at home too, by buying puts on TLT – at the money on long-dated options is trading at an implied volatility of about 16.5% right now. The below chart is the 30-year treasury bond yield.

There have been other prominent people in the Twittersphere piling in (e.g. Harris Kupperman) on the risks of long-term interest rates rising – it’s one way to flatten the yield curve with the short side going longer, it’s another thing completely for the long end of the curve to go up.

In general, when more people are conscious of a particular direction of trade, the riskier the trade becomes. Both Ackman and Kupperman are “talking their book” at this point, the question is whether they were at the beginning of this wave, or whether it’s mid-crest. I’m not sure.

My lead suspicion from a macro perspective is that the market is catching wind that the US Federal Reserve is not going to let up on short term interest rates anytime soon, coupled with the US Government’s Treasury issuing tons and tons of debt financing after Congress approved the rise in the debt ceiling – the US Government is raising a huge amount of cash. Economic data is too strong and employment is surprisingly resilient (with resultant wage pressures). We still see way too much speculative impulses in the market (for a good time, look at American Superconductor – AMSC on the Nasdaq).

What you’re seeing as a result of slow quantitative tightening, the US Government being the first claim on US currency (the treasury auction IS the price on money), and continually rising interest rates is a liquidity drain. As the liquidity gets sucked out of the system, the continual demand for money (the least of which to pay interest on debts) will result in a higher cost of money until the Federal Reserve decides to stop. Because so many have speculated about “the pause”, it blunts the effect of rising interest rates and hence the need to raise rates and tighten liquidity further.

Let’s take the Kupperman scenario of long-term rates going to 600bps, which means a risk-free P/E of 16.7 for significant duration. I’ve pointed out in the past that the risk-free rate is competing significantly against equities and this competition gap will continue to get wider and wider. We would surely see equities without earnings power depreciate. We would also see higher incumbency advantages in capital-intensive existing companies. I also think it would be the straw breaking the camel’s back with certain REITs which are already on the financing bubble (look at my previous post about Slate Office).

The question is whether the US Government, currently printing off massive deficits, would actually be able to taper their spending or whether this leads to another conclusion that we’re going to see massive levels of inflation, much more so than we previously have seen. Will we get to the point where we see defaults and a credit crunch?

Either way, it leads to a similar conclusion – keep a bunch of dry powder (cash) handy for buying into blow-ups that won’t go into Chapter 11 or CCAA. The 5.5% or so of short-term risk-free money is better than nothing, although I too even think this is a crowded trade. For large-cap investors out there, an example of an opportunistic miniature blowup was TransCanada (TSX: TRP) a few days back – although something makes me suspect you’re going to see it go even lower than $44/share in the upcoming months. There are going to be plenty of further examples like this going into the future of companies facing issues with debt.