This is a post without much direction.

Canadian Macro

Perhaps the largest surprise to occur in the past two weeks was the Bank of Canada deciding to resume interest rate increases. I generally believe that this is an attempt to shake up complacency in the marketplace and that we are approaching the point of diminishing returns. By increasing future implied interest rate expectations, however, is in itself a form of interest rate increase. So we continue to have the triple barreled approach – actual rising interest rates, threatened future interest rates, and quantitative easing. Interest rates started rising on March 2, 2022 and we are about 15 months into the program. As capital hurdle rates have increased and projects that otherwise would have been initiated stall out, we’re probably going to start seeing this slowdown occur pretty soon.

The yield curve remains heavily inverted – right now you can get a 1yr GoC yield of 5.07%, while 10yr is 3.40%, a 167bps difference.

GST/HST inputs, from fiscal 2021-2022 to 2022-2023 (table 2), only rose 2.7% year-to-year, which is a negative real growth in GST-able consumption. This does not bode well overall.

I look at the inflation inputs and it seems intuitive that cost increases will continue to rise above the 2% benchmark – especially on shelter. The interest rate environment (in addition to other roadblocks) is seriously constraining supply, yet demand continues to remain sky-high (one of the effects of letting in a whole bunch of people into the country, including students, which massively raises rental rates in cities).

Inefficient spending

One of the problems of using GDP is that it doesn’t account for unproductive expenditures vs. productive expenditures. If you paid somebody a million dollars to move a pile of dirt from one location to another, and then back again, you would have a million dollars added to the GDP, but the wealth of the country has gone nowhere. That money could have been used for something more productive. If you get enough of this inefficient spending, it starts to show itself in other components of the economy – namely demand for goods/services that clearly are not being supplied because you’ve tasked too many people with moving piles of dirt from one location to another and back again. Those people could have been employed in another activity, say road building, which is a more skillful (and productive) use of moving dirt from one location to another.

It is pretty much the reason why much government spending is inefficient – it gets directed to segments of the economy which are for political purposes rather than productive purposes. Do this enough, and you eventually get inflationary effects in the things that people really need.

A lot of what we have seen over the past 15 years or so can likely be attributed to the cumulative effects of this. While governments are the chief culprit, the private sector as well has significant bouts of inefficient capital allocation (e.g. look at the value destruction in the cannabis sector, or most cryptocurrency ventures, etc.). The “slack” of the misdirection of resources has been exhausted after Covid, and the cumulative impact is truly obvious – a lot of people are going to suffer as a result, and collectively our standard of living will be declining.

Nifty 50 re-lived

The nifty 50 were the top 50 stocks in the US stock market in the 1970’s. Today, the top 10 stocks of the S&P 500 consist of about 30% of the index and many comments have been made about the effect of these stocks on the overall index. In particular, the rebound in technology stocks since November 2022 has caught many fund managers by surprise, and it is to the point where essentially if you did not own them (Facebook/Meta, Nvidia, etc.), most closet index fund managers would have badly underperformed. Perhaps it is sour grapes from somebody like myself (where I am barely treading water for the year), but this just does not look healthy.

Safe returns

Cash (various ETFs) return about 5.08% at the moment. For yield-based investors this is a very high hurdle. For example, looking at A&W Income Fund (TSX: AW.UN) with its stated yield of 5.3% – while you do get a degree of inflation protection, how much can burger prices rise before you start seeing volume slowdowns (and it is volume, not profitability that counts for these types of royalty companies)? Cash is out-competing much of the market right now. With every rise in the short-term interest rate, the differential widens.

Everybody looks at the charts of long-term treasury bonds in the early 1980’s and said to themselves “if only I had gone all-in on those 30-year government bonds yielding 15%, I would have made out like gangbusters”. This is almost the equivalent of saying your ideal timing into the stock market is February 2009, or March 23, 2020. The problem with such statements, other than they are entirely “hindsight is 20/20”, is that in order to get those 15% yields, such a bond needs to trade at 10%, 12%, 14%, etc., before reaching that 15% point. Valuations that would seem attractive and bought before that 15% yield point will have unrealized losses, sometimes significant, at the crescendo event. This is usually the point where most leveraged players are forced to be cashed out at the violent price action.

Parking cash is boring, and likely will result in the loss of purchasing power over periods of time (the CPI is a terrible barometer for ‘real’ consumer inflation), but better to lose 5% of purchasing power instead of 40% in a market crash!

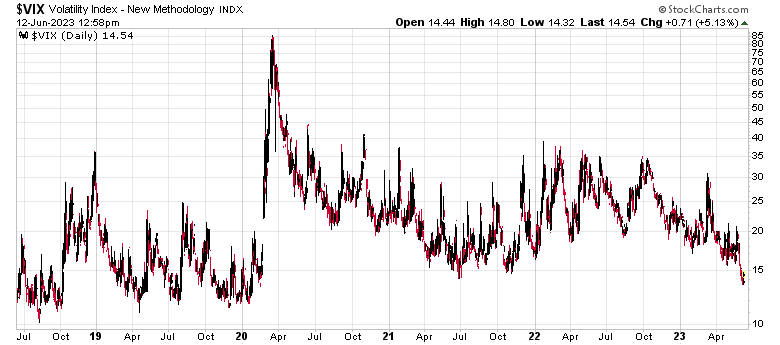

Implied volatility

The so-called ‘fear gauge’ (the 1-month lookahead volatility of the S&P 500) is getting down to 2019 lows:

I don’t know what to make of this. Markets price surprises and probably the biggest surprise is a rip to the upside, despite all of the doom-and-gloom that the macro situation would otherwise suggest – perhaps interest rates are going to rise even further than most expect?

Either way, I’m not going to be a market hero. I remain very defensively postured and I do not feel like I have much of an edge at the moment. When you had everybody losing their heads over Covid three years ago there was a ripe moment where the reality vs. psychology mismatch created huge opportunities. Today, the normalization of this reality vs. psychology has created much more efficient market pricing. I can’t compete in this environment which feels like trading random noise. Maybe the AIs have whittled away the differential between reality and psychology – but they are only as good as the data that gets fed into them, and markets tend to exhibit random patterns of chaos now and then which will throw off the computers. So I wait.

If you ever wonder why I can’t work in an institutional environment, it is due to having some radical thoughts like the last paragraph.