Even though one would think with the S&P 500 and TSX being at heights that I would find the markets devoid of investment opportunity. While the Amazons and Facebooks of the investment world do appear to be expensive (and entirely propelled by deficit spending, federal reserve meddling, low interest rates and a good dose of TINA), the smallcap world, much to my surprise, has been full of plenty of research candidates, both old and new. I’ve been doing due diligence on various companies over the past couple months and have nibbled here and there. Nothing was as obvious as Yellow Media was in the 6’s in early 2019, but several items have received my interest and present reasonable risk/reward ratios.

I will write and disclose one of them simply because I have gotten my position (it is a very low percentage position in the portfolio, as in my minimum size to warrant opening anything) and I am not interested in accumulating more at lower prices. I will also caution that its liquidity is less than stellar.

I will piggyback on the post Tyler did with FP Newspapers (TSXV: FP) – well worth the read – he did a good job. Just be warned if you trade FP that you can move the stock price 20% with a few thousand dollars of volume!

It is well known that the traditional news publishing industry has been upended by the internet. Even Warren Buffet was caught flat-footed by this to some degree (he has made multiple comments on two-decade ago annual reports about the competitive position of single-community newspapers). However, I will make the claim that most of the damage in the industry is done. It is not completely over but the horizon is finally visible again.

In terms of publicly traded companies in Canada (on the TSX), we have the following:

* Torstar (TSX: TS.B) – notably owning the Toronto Star, Canada’s largest daily newspaper. Will write about them in more detail below.

* Postmedia (TSX: PNC.A / PNC.B) – National Post, and many prominent regional media, including the Vancouver Sun, Calgary Herald, Toronto Sun and Montreal Gazette. The stock, despite having over 90 million shares outstanding and a $120 million market cap, is very illiquid. They have an anchor around their neck in the form of nearly $250 million in debt and mandatory cash sweeps, contrasted with the trickle of operating cash flow they do generate.

* Glacier Media (TSX: GVC) – Owner of some 60+ local news media brands, although this is a subset of their other significant business offerings. Unlike Postmedia, the stock usually trades in a day, and the bid-ask spread is much more reasonable (pennies vs. dimes). Their Community Media category (which includes publications such as the Victoria Times Colonist) is approximately 60% of their revenues. They have been treading water financially, and have a very modest amount of debt on their balance sheet (about $20 million). They are, practically speaking, controlled by the entity that controls Madison Pacific (TSX: MPC.C).

* Québecor (TSX: QBC.A / QBC.B), which also owns the major French language publication (Le Journal de Montréal) and others in French language. Québecor is well diversified beyond its ownership of newspaper publications (its ownership of Videotron, for example) and really doesn’t fall into the “trading like trash” category of the three companies listed above.

I’m only going to look at Torstar in this post. This post has less quantitative rigour than my usual posts but I’ve done those evaluations off-line. Also, I’ve been less than comprehensive in writing the following analysis, but there have been plenty of other considerations taken into the scope of this.

Structure

The company has a dual class share structure. Its original founder and owner, Joseph Atkinson, who died in 1948, left behind the company to his successors who own the Class A voting shares.

The Class A shares (approximately 9.8 million outstanding) have voting rights, are not publicly traded and are owned primarily by a voting trust that joins together seven groups of shareholders. These seven groups (descendants of Atkinson) collectively hold approximately 99% of the Class A shares of Torstar and approximately 17% of the Class B non-voting shares of Torstar. They effectively control the nomination of the board. Class A shares can be converted into Class B shares. Class A shares cannot be sold in a take-over bid unless if the same offer is given to Class B holders.

The Class B shares (approximately 71.3 million outstanding) are freely traded, and notably Fairfax owns 28,876,337 shares or 40% of the class. Their last disclosed purchase was on November 9, 2017 when they purchased 9.4 million shares at CAD$1.25/share.

This dual class structure looks fairly typical, except for the following provision:

The holders of the Class B non-voting shares are generally not entitled to vote at any meeting of the shareholders of the Corporation; provided that, if at any time the Corporation has failed to pay the full quarterly preferential dividend on the Class B non-voting shares in each of eight consecutive quarters, then and until the Corporation has paid full quarterly preferential dividends (7.5 cents per annum) on the Class B non-voting shares for eight consecutive quarters, the holders of the Class B non-voting shares are entitled to vote at all meetings of the shareholders at which directors are to be elected on the basis of one vote for each Class B non-voting share held.

This creates a control incentive – the company must pay 15 cents per share in two year periods, otherwise Class B shares will get to vote for board directors (i.e. Prem Watsa will be able to obtain significant influence, if not control of the firm – his voting stake in this instance would be 36%).

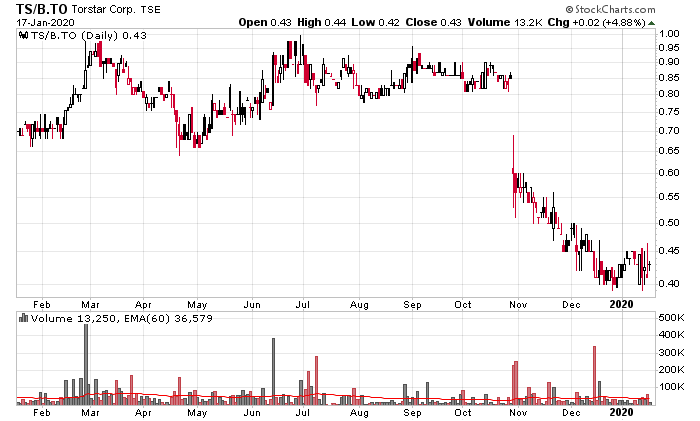

The bulk of my shares were bought at 40 cents, which means if the Torstar board wishes to keep control, they have to pay a minimum 18.8% dividend at this cost.

On their Q3-2019 report, Torstar eliminated their dividends (it was 10 cents per year prior). You can see on the chart when this announcement occurred.

The board of directors stated they will review the dividend policy again in a year. I do not believe they will reinstate a dividend until there is obvious evidence of free cash flow, or Q3-2021, whichever comes first.

Financials

The following is a very broad summary. I’ve dived into the financial statements, but will pick on certain details. Print advertising is eroding at a very fast pace (roughly 23% from Q3-2018 to Q3-2019), and flyer delivery (which used to be a vector for advertisers to stuff more paper garbage into doors of homes that competed primarily with Canada Post’s unaddressed admail) is down 10%. Digital advertising and subscriptions are roughly level.

I do not expect there to be much recovery in print, but because revenues have already fallen so much, one can envision that the inflection point on the inverse “S” curve has been reached and that future revenue erosion will be slowing. Print advertising is still 30% of the total revenues. All of the advertising money has to go somewhere, and it is likely it will show up in the form of digital advertising (either on Torstar or thrown to social media), or “advertorials” and the like.

With revenue losses, cost containment becomes a much more challenging factor, and management has been trying to trim costs. For the most part their effort has not been sufficient in line with the drops in revenues, and there have been recurrences of “one-time” restructuring costs and so forth (the most recent going to be the shutdown of the StarMetro line of publications).

The other big component is the partially consolidated 56% ownership of Verticalscope, which is generating losses and the subsidiary has a $144 million debt which it is slowly chipping away at. Torstar has been less than transparent in terms of accounting for this investment, probably because it has performed so terribly. They were forced by the Ontario Securities Commission to change the manner in how they reported VerticalScope results. For the gory details, you can read Note 8 of the financial statements and the beginning of the MD&A document.

The consolidated balance sheet itself, however, is not in bad shape. The company has $52 million in cash, $9 million in restricted cash held generously in allocation toward an executive retirement liability, and no debt (the VerticalScope debt is non-recourse). There are significant liabilities on the books in the form of the employee pension plan, which is estimated to have a $127 million solvency deficit as of September 30, 2019.

This number might be a little scary, but it is not as if the pension plan is devoid of assets – at the end of 2018, there was $806 million in pension assets. There were $77.6 million in benefits paid that year.

The main point is that the company has some financial maneuvering room and time to work with. While the situation is clearly adverse, it is not at the point where it encumbers management’s ability to operate (unlike Postmedia, where the high interest rate debt is like an anchor around the neck of the whole company).

Intangibles

The large intangible aspect that makes Torstar alluring is name recognition – being a major media driver in itself, with obvious critical mass, provides value. There are analogs to this, the most relevant one being the decision that Jeff Bezos made when deciding to purchase the Washington Post in 2013.

The other intangible aspect is that the Toronto Star is obviously aligned with the federal partisan leanings of the existing government, which means it will continue to be a receptive economic vessel for the federal government. The journalism tax credit is one instance of this.

Competition

Direct competition – The Globe and Mail (owned by another historical family-owned media empire, Woodbridge Company) is the only other direct competitor in this space. They are effectively the two legacy national (English language – Québecor owns the French one) newspaper organizations.

Other than this, the other competition is through other domains – broadcasting news, internet, and independent publishers. The combination of these three has lead to a non-trivial erosion of the fundamental business, but this has been well explored elsewhere.

Sentiment

Bad. Really bad. Other than the negative dynamics of the newspaper industry, the suspension of the dividend was probably the last nail in the coffin for a lot of investors to finally bail out. I do suspect a lot of the trading since that announcement was fueled by tax loss selling. Q4-2019’s result is probably going to be quite poor with costs associated with shutting down StarMetro and there isn’t any good news at all other than the federal government subsidizing the business with digital media and journalism tax credits.

Valuation

The company’s Class B shares traded last Friday at 43 cents per share, which gives it a market capitalization of $35 million. In happier times (in 2011) the company traded as high as $15/share. It has spent most of 2019 under $1, and so far in 2020, it has been under 50 cents.

The question at the end of the day is whether the entity can sustainably generate cash. I believe the answer to this is yes. The question is how much the underlying business has to shrink in order for them to get to that point, and whether management can execute on structuring a leaner organization to doing so. That remains to be seen, but things right now are priced for a huge amount of pessimism relative to their market capitalization. The range of outcomes in my books are them going slowly to zero to being able to recover to a much higher market capitalization – when using a linear probability curve, the expected value is higher than 40 cents per share.

The big kicker is the ticking clock on dividend payments, which I think will give the board of directors incentive to tell management to get going. In the event they want to save themselves, they will give a 15 cent per share dividend by Q3-2021, which will mean I at least get paid to wait. If not, I’m sure Prem Watsa will have better ideas.

To repeat, I have a very small position in Torstar. If they pull off a miracle and get back to a $250 million market capitalization, it will be a welcome boost to the portfolio. If it’s clear that things are going from “really bad” today to “really really bad with no hope”, I’ll take a couple lumps on the head but it won’t cripple my portfolio by any extent.

If you do trade this, be warned that liquidity is not the greatest. It typically trades around $10,000 in volume a day, and the 2 cent spread you typically see in the stock represents a 5% price difference so selling at the bid and buying at the ask is very expensive if you are impatient!

My thoughts exactly. What I learned–or hope I learned–in FP Newspapers is that sentiment is paramount.

I was probably 5-10% of the volume in FP in 2017-8, and ended up basically flat on the investment because I had the wrong thesis (that eventual distribution reinstatement would be the catalyst for market attention) and, I think, a poor understanding of the (vanishingly tiny) market for the security. Sentiment took a very long time to turn after performance began to stabilize (which is to say, deteriorate at an acceptably slower rate) and after the govt hinted it would subsidize the industry (even with uncertainty of what form the subsidy would take, and whether it would be enacted/enactable, I was shocked that newspapers didn’t shoot up on the news).

Anyway, I think you’re spot on (of course, because we agree!) in Torstar. Its (relative) liquidity, marquee name and somewhat-harder deadline all make for a very interesting investment. And somebody could write a book about the fleecing of (willing, eager) legacy newspapers by sellers of new-media marketing/social/analytics companies in the past decade.

Uncle Warren throws in the towel on his newspaper empire:

https://www.bloomberg.com/news/articles/2020-01-29/warren-buffett-throws-in-the-towel-on-his-newspaper-empire

“Berkshire Hathaway Inc. agreed to sell its BH Media unit and its 30 daily newspapers to Lee Enterprises Inc., which owns papers including the St. Louis Post-Dispatch, for $140 million in cash. Lee has been managing the papers for Buffett’s company since 2018, and Berkshire is loaning Lee the money for the purchase.”

…

“Berkshire is lending Lee $576 million at a 9% annual rate for the purchase and to refinance other debt. Excluded from the sale is BH Media’s real estate, which Lee is leasing under a 10-year agreement.”

Yup. Their choice to slide from equity to debt is an interesting data point.

Over the past years, I have looked at FP Newspapers and could never get myself to buy into the company. One question I ask myself is, “If FP were to fold tomorrow, would the world notice?” In my humble opinion, I have come to the conclusion that the answer is “No.” For instance, in the case of FP, I have always believed that they owned subpar assets and that the corporate structure was tilted against the public shareholder: FP Newspapers, Inc., the publicly-traded entity, owns units of the “FPLP” (FP Newspaper Limited Partnership), thereby entitling it to distributions. To problem with this structure is that control is unattainable for public shareholders and is in the hands of management who may have incentives and interests contrary to those of public shareholders.

As far as Torstar is concerned, the problem is that business is up against extreme headwinds. In reality, similar to FP Newspaper—and this is only my humble opinion—I do not believe that the world would care if Torstar were to fold tomorrow. The reality is: If the news information business is moving from print to digital form—and it is, at accelerating pace—the question one needs to ask is, “Where is the consumer going to get their digital news from?” Granted, the news publication industry may not be entirely on its way to the graveyard, but Torstar is, one needs to remind oneself, a publisher of general news. This isn’t a specialized publication that can handle the transition from print to digital in an easier fashion (the specialized publisher has a more “sticky” readership). (Think Foreign Affairs. National Geographic. Time Magazine. The Economist. The New Yorker.) In the case of Torstar, its readership could easily transition to getting news from their Twitter or Facebook feeds, for instance, whose algorithms can bring the most interesting content before the reader’s eyes and whose feeds can be tailored to the reader’s interests. No matter how “great” Torstar manages to pull the online transition, it’s still a generalist publication—granted one with a liberal stance, which stands for progressive values et cetera—but so is most online news platform these days. Again, where is Torstar’s moat? In my humble opinion, I just do not see it.

Another thought provoked while reading your article was that this is another of these turnaround stories, and frankly, turnarounds are difficult to execute. I personally prefer to put my money in industries that have far greater prospects than into a stock such as Torstar which is up against nasty forces ravaging the industry. Or alternatively, to put money into stocks of “okay” businesses at attractive valuations with very limited downside (my current strategy—with over 88% of my portfolio into a single stock).

Anyway, these are just some of my thoughts on Torstar, which frankly I haven’t looked at in 6 months and FP Newspapers which I haven’t looked at in about a year. Thank you Divestor for sharing this post and to the commentators for sharing their thoughts. The quality of analysis and discussion on this site has been nothing short of stimulating.

This is a very well thought out comment. My brain had to brew on the answer for a couple days.

The “If FP were to fold tomorrow, would the world notice?” type of question is always very subjective. Perhaps a better way of phrasing it would be “would the world care?”. You use the word ‘care’ later in your discussion so I’ll incorporate it here. In the case of FP, I think a better question would be “would the people of Winnipeg notice/care?”. I’ve only spent a couple cold days in February in Winnipeg in my life, so I wouldn’t know.

About Torstar, while I think Toronto (and Canada) would survive, I definitely think it would be noticed. Probably celebrated by Conservatives (“typical left-wing media got what it deserved and lost its readership by being so partisan”) and lamenting by Liberals (“government should have subsidized them more!”) if it happened. The moat for generalist news, is incumbency. Not a very strong moat when you have numerous examples down south chipping away at news niches, but up here in Canada, I’d claim that Toronto Star’s niche is left-leaning friendly news. Can getting a readership across a sixth of Canada be easily replicated? Not so easy.

Turnarounds are difficult and rarely clean and never go to plan. A difference here is that Torstar’s balance sheet isn’t a gong show (compared to Postmedia at least) and was trading very cheap, coupled with the “pay dividends in two years, otherwise you lose control” hammer.

One other question… 88% in a single stock? I am very curious about this conviction.

Today’s action: Took about $35,000 of trading to get the stock up from 43 cents to 50 cents a share.

8-page advertorial on the Toronto Star today on private schools. The politically correct name for this is “Supported Feature”. The future of media – ‘news’, ‘opinion’, ‘advertising’, ‘entertainment’, and all of it completely indistinguishable from each other!

They have the distinction of trading for quite a bit less than the cash on their balance sheet, assuming the sale of the Hamilton building goes through.

They’re a bit like a biotech: either the market cap catches up with the cash, or the other way round.

Their Verticalscope acquisition was a bit of a disaster but fortunately they still continue to generate some cash, although makes you wonder whether they can pay off the debt there.

Otherwise I thought the Q4 report was actually quite good all things considered. It reminds me of a patient trying to clot a gushing wound and achieving partial success. The question is whether they’ll be able to keep cutting those costs and managing such businesses is never easy.

Agreed. Looks like we’re in for many more one-offs, but even mild and partial signs of bottoming out are pretty good news in this context. Remains a story, investment-wise, for 2021 (so long as they don’t blow anything up in interim).

I can’t imagine workplace morale is very high, and the less said about Verticalscope the better.

Looks like I picked the wrong newspaper! Torstar bought for $0.63.

https://finance.yahoo.com/news/nordstar-capital-acquire-torstar-corporation-235400047.html

https://divestor.com/?p=9645 Wrote about it here.

[…] January, which felt like a very long time ago, I wrote about Torstar. In fact, at one point I owned shares in the company, but during the CoronaCrisis, I dumped my […]