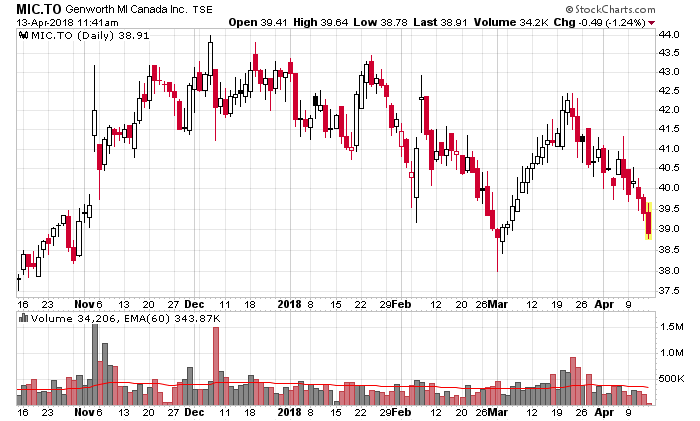

Genworth MI (TSX: MIC) has taken a hit over the past three weeks due to statistics that housing sales and average prices are declining nationally, according to a CREA report. Another sensationalist headline (“Canada’s average home price drops over 10% year-over-year in March”) is here.

Genworth MI stock rose in the month of March partially due to the company going on a buying spree on a stock buyback – it bought back 1.2 million shares. Other than that, there has been consistent selling pressure.

The report cites the impact of the B-20 regulation from OFSI, which increases the qualification criteria for people to obtain non-insured residential mortgages.

There are two factors here as it relates to Genworth MI that are being confused: 1) the pool of potential insurable mortgages, 2) what exactly the implication of average pricing statistics entails.

Aggregate Statistics

What market participants are failing to understand is that statistical averages fail to capture the economics of the mortgage insurance market, even in a declining average price environment and are probably taking down the stock due to incorrect reasoning (which usually leads to an environment where the stock will be undervalued).

The national housing price statistics are dominated by three regions: Toronto, Montreal and Vancouver. The “right-side tail” of the distribution of housing prices in the Toronto and Vancouver markets (especially in single-family residential) are dominant factors in statistical mean pricing. For instance, if your housing market consisted of a $3 million house, a $1 million townhouse and a $500,000 condominium, a 10% decrease in the house price would dominate over a proportionate decrease in the townhouse or condominium price, due to price weighting.

Vancouver is an extreme market, partially due to the huge influx of foreign capital buyers, which the government is actively trying to curtail. The 95th percentile of the real estate market is dominated with speculation from foreign (mainly people connected to Mainland China) buyers and asking prices have been decreasing in the hundreds of thousands of dollars for single family dwellings in the Metro Vancouver region. I have been paying less attention to the Greater Toronto Area, but apparently there is a similar mechanic going on there.

As a result, when speculation moves the 95th percentile market, it will result in massive price swings that have powerful effects on aggregate mean statistics. There is a “bubble-down” effect on the remainder of the real estate market, but this is more diffuse and domestic demand for lesser priced properties serves as a buffering effect for the absolute decline (not percentage decline) in those prices. It pays to longitudinally study properties that are in the 50th percentile (i.e. using median statistics) as a more intuitively accurate grasp of what is going on. These usually aren’t published.

Mortgage Insurance Eligibility

Keep in mind that properties over $1,000,000 are not eligible for mortgage insurance. Secondary residences in Vancouver, Calgary and Toronto are up to $750,000. (Good luck with this amount in Vancouver!).

Net Impact to Genworth MI

The only impact I would expect from what is happening in Vancouver and Toronto is that less mortgage insurance will be written – this is derived from the decrease in re-sales of real estate. The quality of the underlying insurance portfolio will also exhibit a higher loan-to-value ratio as prices normalize, but as mortgage insurance services the more “retail” element of real estate purchasers, I would expect them to continue paying their mortgages and amortize the existing debt amounts – 15% of the debt is amortized in 5 years with a typical 25 year amortization period and 3% interest rate. Employment is a much bigger driver – I would worry if unemployment rises.

Genworth MI will report the first quarterly report in late April or early May – I would continue to expect to see very good numbers posted with respect to loss and severity. Book value should also creep up another 60-70 cents per share, which would bring it close (but not quite) to $44. At the current price of $39, they are trading at a moderate discount.

Genworth’s timing of buyback has been so-so to say the least.

@Will: They paid roughly $41/share average and were fairly indiscriminate at hammering the market during their buyback period. Not the best trading for sure.

What would cause you to change your view on this co? Increased unemployment? Median price declines?

Thanks

@John: I’d really start to worry if forces eroding CMHC’s pricing power started to emerge.