Genworth MI (TSX: MIC) reported their 4th quarter results today. For those new here, I’ve been freely covering this company for ages. It is the stock in my portfolio I have held for the longest period of time (since 2012). It has sometimes been the highest concentration position in my portfolio, but it currently is not. Here are some notes:

1. The big headline-grabber should be the loss ratio. It is still exceptionally low (9%) – reflecting a relatively stable real estate climate. The average loss ratio for the fiscal year was 10%. This is at a record-low level.

Let me put some context to this. The loss ratio means that for every dollar of insurance the company recognizes revenues on (note this not the insurance they write in a given year although the two numbers are correlated), that the corporation books 10 cents on the dollar of expenses because they have to account for losses on insurance claims.

This means for every dollar the company recognizes, they retain 90 cents, before other expenses.

The expense ratio is 20%, which means it costs 20 cents on the dollar to administer the insurance (e.g. commissions paid to acquire the policies, the administration of claims, management, etc.).

So what is left over is 70 cents on the dollar.

From this pool of money, the two big expenses left to be paid is interest on debt and income taxes. $24 million was booked for interest expenses (about 3.5 cents) and $188 million (28 cents) was booked for the year in income taxes.

However, (this is where readers of Warren Buffet’s annual reports will know this on the back of their heads), Genworth MI has the benefit of float, which is the 6 billion in assets they have to invest before they pay out claims. As a function of premiums recognized (revenues), Genworth MI made 39 cents on the dollar with their investment portfolio.

So when you do the math, the company recognized $676 million in revenues, and recorded a bottom-line amount of $528 million, or 78 cents on the dollar of net profitability.

I want anybody to tell me any other company on this planet earning 78% net margins, after interest, depreciation/amortization, and taxes.

When people are paying their mortgages, this is a wildly profitable industry to be in.

This breaks when people start defaulting on mortgages, causing a collapse in real estate pricing due to forced liquidations, and then soon mortgage insurance providers will be hard-pressed to pay banks that will be knocking on the door. So far, this scenario has not happened. A rising real estate price environment means that even when people default on their mortgages, when they occur, such defaults are not severe from a mortgage insurance perspective – even when there is fraudulent underwriting (see: Home Capital Group).

The Canadian government is most unlikely to change this insurance scheme, because the 100% government-owned crown corporation, CMHC, is also raking it in – their volume is roughly double of what Genworth MI does. Why interrupt the gravy train when this crown corporation is delivering huge amounts of cash to the government in the form of mortgage insurance fees?

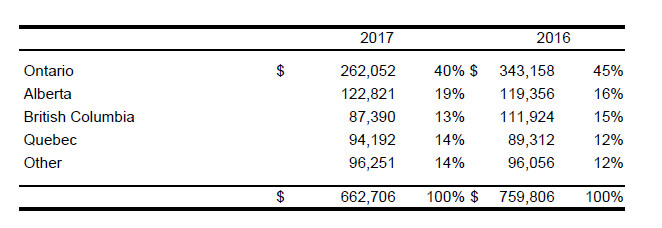

2. Premiums written on transactional insurance was up slightly from Q4-2016 – mainly due to the increase in mortgage insurance rates from last year, offset by decreased volume due to mortgage rule changes. Portfolio insurance is down significantly, but this was expected due to regulatory changes. My take on this is that it appears that the dollar amount of insurance written has stabilized. There is slightly less concentration in Ontario/BC than the rest of the country:

3. The interest rate swap they took to the tune of $3.5 billion notional value 3-5 years out continues to pay off – fair value of $131 million at Q4-2017 vs. $120 million in Q3-2017. This was a very, very smart move on interest rates.

4. In terms of balance sheet management, the only changes to the portfolio has been a slight shift away from corporate debt, in favour of collateralized loan obligations and an increase in corporate preferred shares (5-year rate resets). Fair value has increased to $6.45 billion from $6.34 billion.

5. It is still not entirely clear what the impact of the China Oceanwide merger with Genworth Financial (NYSE: GNW) will be – or even whether this merger can be consummated at all. Reading Genworth Financial’s 8-K, a huge stumbling block is “The delay in the review process is due to the difference in opinion of the fair market value for Genworth Life and Annuity Insurance Company (GLAIC)” which is a huge stumbling block (this subsidiary of Genworth Financial is saddled with liabilities concerning the long-term care insurance pricing disaster). One potential scenario has always involved Genworth Financial completely selling off their holdings of their Australian and Canadian mortgage insurance subsidiaries.

Genworth Financial is also looking at a secured bond transaction to finance their upcoming 2018 bond maturity – although they have the cash at the holding company level to pay it off, it will leave them constrained.

6. Minimum capital test level is at 168% with the target being 160-165%. Management has a history of either executing a share buyback or giving out a special dividend with the excess capital. Their history has typically been quite prudent and only buying when the stock is at a substantial discount to book value – which it is not presently. I would believe they will be holding tight and figuring out what to do with the excess capital later. Diluted book value is $43.13, while the common stock closed today at $41.49.

(February 7, 2018: Listening to the conference call, I believe management will let the MCT go substantially higher than 165% during 2018 – I no longer believe a share buyback or extraordinary dividend will be in the works in 2018).

(April 9, 2018: My February 7, 2018 note was obviously wrong – the company bought back 1.2 million shares in March at around $41/share).

The company remains in what I consider to be my fair value range at present.

[…] about my position in Genworth Mortgage Insurance Corp, the biggest reason being I feel that what Divestor has posted about it is better than anything I could write. It’s a controversial stock, as many think […]