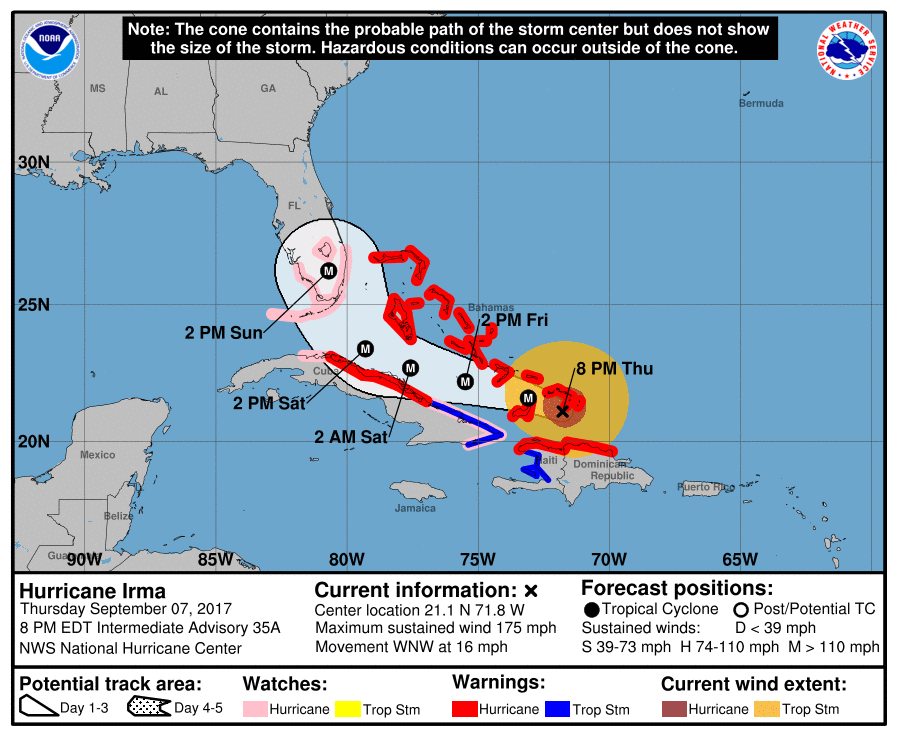

Hurricane Irma is looking like it will blast a path through most of Florida in just over two days:

The media is making it look like that it will be apocalyptic. Indeed, the island St. Martin (famous for having an airport where you can sit on a beach and look up about 100 feet and see a landing Boeing 777 jet) was nearly annihilated. Right now Irma is one of the strongest (if not the strongest) in recorded history, but the question is where it will strike landfall in Florida (if there) and how much it will dissipate by that point – 75 miles can make a material difference in the damage calculation. If it goes through the heart of Miami, there will be tons of damage, but if goes through the western part of the peninsula, there’s a decent chance that the winds will slow down sufficiently by Tampa to still cause a lot of damage, but not the insane amounts the media is making it to be.

Thus while the media hype is overwhelming, the markets are treating certain insurers like the catastrophe is already a done deal, which may not be the case.

This is the classic information mismatch that creates market opportunity.

Larger insurers can take the hit (most likely), and smaller, Florida-centric insurers like UVE have been grabbing the proverbial nickels before steamrollers. Even though the latter group is down quite a bit (something which started well before Irma), it’s debatable they have a sustainable business model, which is why many have been working to diversify away from FL and from simple property insurance. I’d rather own a large insurer at .7 alleged book still recovering from a host of sins and crises than a small, mostly single-state insurer at 1.4 book that’s been riding headwinds for nearly a decade. Still, talk about “too hard”!

My preferred insurer (investment-wise) is trading up today after it started much lower. The initial opening price never got to my desired price.

This is probably because the storm track is tracking west so Miami is saved from a major hit. It will be bad for them but not catastrophically bad.

Tampa seems more vulnerable but when the hurricane makes landfall, the energy dissipates and it’ll be category 1 at that time (bad, but not terrible).

& so on to the next storm!

Also, TBL has become more interesting, though I suspect still not your thing. They are looking into calling and refinancing their notes, which they can do as of 9/1. They’re currently paying 14%, a crisis rate; every 1% reduction in the rate will result in (pre-fees, etc.) ~$1.2 million annual savings. They’re not a super-cheap stock (~7.5 LTM EV/EBITDA; ~7x PE on avg E of last decade), but with successful refinance could be at an inflection point where benefits begin to accrue more, and significantly, to equity. TBD.

Hi Sacha

Your “subscribe to comments without entering one” is not working….(about a week now).

@Aharon: I gave up on trying to figure out TBL after they bought back their note issue many, many years ago. Now I just look at them and figure out why their interested insiders have such deep pockets.

@Marc: I was using a comments subscription form that came from the ice ages, and I’ve upgraded the mechanism and it also supports the “I want to subscribe to a comment but not post” feature. Give the new one a spin now and let me know (sacha@divestor.com or comments) if it doesn’t work. Thanks.

Sacha…the emailed verification is not hyperlinked….you must cut and paste….not a big deal, but thought I would let you know.

@Marc: Is your email provider not automatically hyperlinking it? On a test gmail account, it hyperlinks it…

the hyperlink is not working with yahoomail……this most recent comment notice was not hyperlinked either.

@Marc: I have used my rudimentary HTML skills that were state-of-the-art in 1994 to fix this issue. It turns out that Yahoo mail doesn’t automatically hyperlink what it detects to be URLs (probably due to some spam prevention mechanism or from non-whitelisted email addresses). So it now works and I’ve tested it – let me know if there are any bugs in the future.

To keep this comment on-topic, apparently loss damage from the hurricane is less than a quarter of what they were anticipating ($50 billion vs. $200 billion estimated) and not surprisingly insurers are rising today. I am very sorry to say that despite getting the whole story correct I was not able to execute on anything in the markets with regards to this event. Should have just bit the bullet Friday and hit the buy button.

That seems to have fixed it….thanks