Most people are familiar with the Toys R Us franchise of stores – they sell toys and baby stuff. The Wikipedia entry has a good summary.

Their equity is privately held, but they are still required to report publicly because of debt covenants.

Their financial summary is more grim. They are being slaughtered by Amazon and other online retailers, so their heavy physical presence is causing an erosion of sales and pricing power to the point where they are no longer making money during most of the year.

For instance, from the end of January to the end of October (9 months) in both 2016 and 2015, the company does not make money when factoring in amortization (those physical stores and logistics still need upkeep). The interest bite takes an even bigger chunk out of the corporation.

So the Black Friday and Christmas season is critical. It makes the whole year worthwhile in terms of profitability. Even then, in the past couple years it has not been enough to offset losses of the previous 9 months (In 2016 even when factoring in CapEx and interest, they were slightly short of generating cash).

For the most recent holiday season, same-store sales in the all-critical Black Friday and Christmas period were down 2.5% in the USA and more so internationally. This clearly is not a good trend, and one has to ask whether it will continue or whether it was a one-off thing.

I’m ignoring the fact that their balance sheet is a leveraged mess.

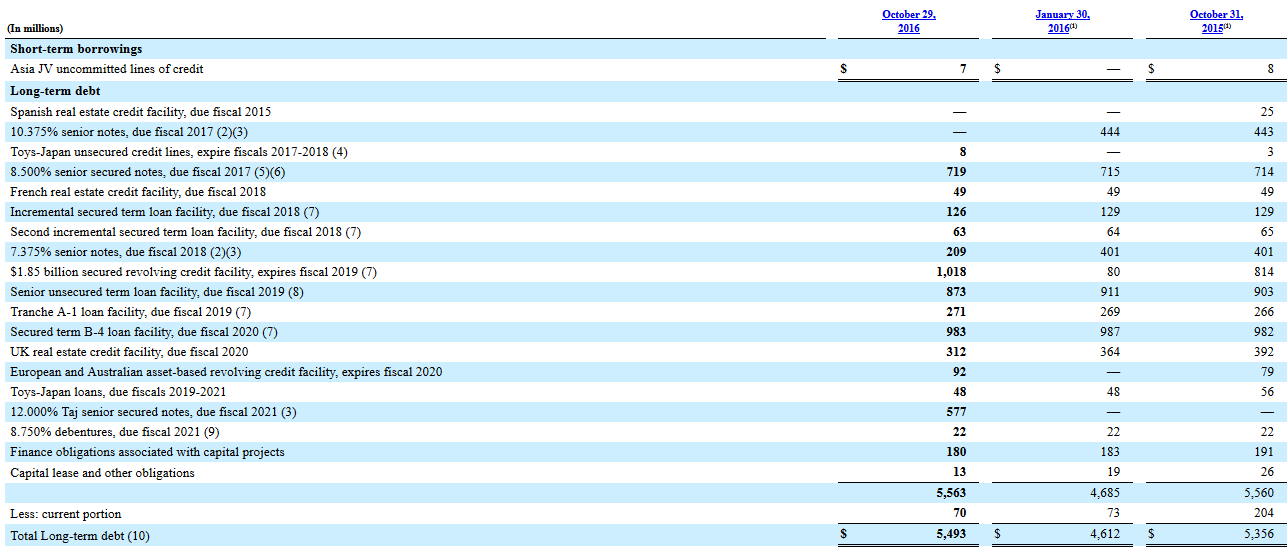

Looking at their latest 10-Q, we have an entity in a negative equity situation (negative 1.6 billion), $420 million cash on the asset side and $5.5 billion in long-term debt.

This is a huge mess. The vast majority the debt is secured. There are convolutions of financings behind the various corporate entities under the holding firm, but suffice to say, it is about as leveraged as things get without getting recapitalized. I believe a recapitalization is inevitable.

Somehow, in August of 2016, they managed to convince the 2017 and some of the unsecured 2018 debtholders to exchange their debt for senior secured notes maturing later in time.

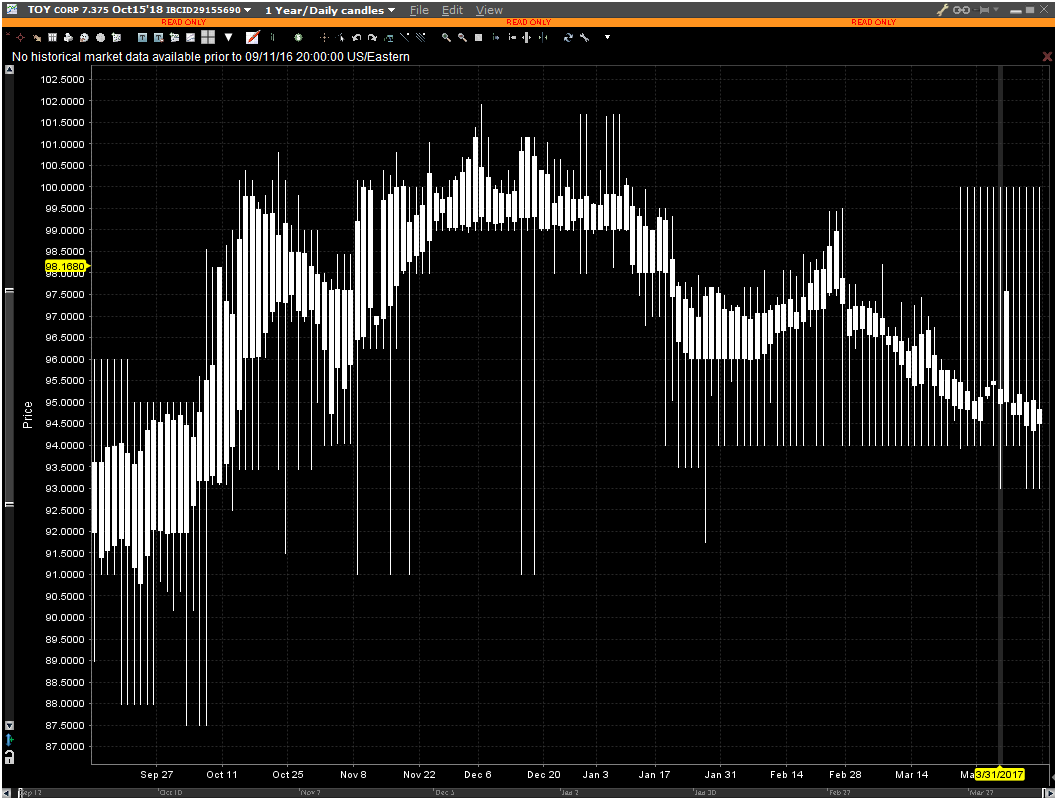

It is the 2018 unsecured notes (7.375% coupon) that I was looking at. They mature on October 15, 2018 and there is US$208 million outstanding (about half decided to exchange their debt for 90 cents of par value of secured debt).

The following is a chart of their trading since the exchange offer was floated:

The debt, at the asking price, has a yield to maturity of 11.3%, and a term to maturity of 1.52 years.

This looked like a Pengrowth-ish type situation where you have unsecured debt that may trump the secured debt on the basis of maturity, rather than security. There is a credit facility that has around $630 million remaining that could pay the October 2018 maturity.

Sadly, the risk of a spontaneous credit meltdown is preventing me from purchasing the unsecured debt. One can also make a legitimate case that Toys R Us will burn through enough cash to prevent them from paying off the October 2018 unsecured debt (they have to accumulate inventory for the that Black Friday / Christmas season and this will be when they need the capital the most).

Hence, I will pass purchasing this debt. I’m going to guess it will trade lower over the next 18 months.