Industry Canada maintains a list of companies going into creditor protection (CCAA).

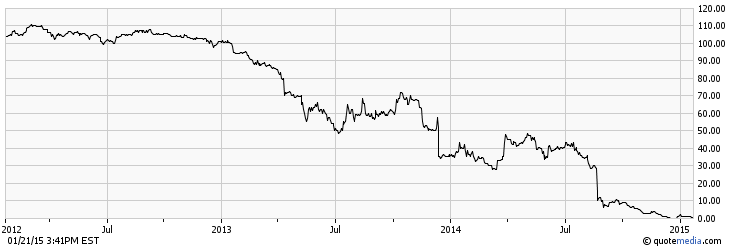

Other than Target Canada (which is for wholly different reasons than the oil market!), GASFRAC (TSX: GFS) has the dubious distinction of going into CCAA first. Their insolvency can be described as operating losses (helps to have a permanent CEO running the company to execute a turnaround!), combined with lack of liquidity (their operating line of credit was nearly exhausted in their Q3 report).

They had a debenture issue which was still trading at a relatively high level (36.5 cents on the dollar) when they finally pulled the plug.

The debentures were supposed to mature on February 2017, and had a 7% coupon and were convertible at $10.50.

The debentures are not that badly far behind in the capital structure – the credit facility is $28.6 million and the debentures are a $40 million issue. Debenture holders may get a few pennies from the firesale.

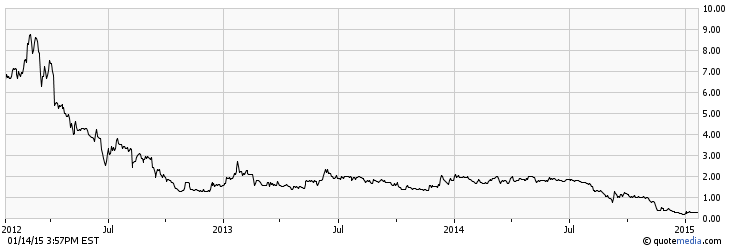

Another recent CCAA filing is Southern Pacific Resource Corp (TSX: STP). They are a pure oil and gas producer and markets were predicting the demise many months ago:

This was an issue maturing June 2016, 6% coupon and if you purchased it at its 52-week low of 0.1 cents on the dollar and the bond matured, it would eclipse making a leveraged bet on the CHF/EUR pair before the Swiss bank announced it was removing its Euro peg.

Other companies I’m waiting for to hit the CCAA bucket include:

– Arcan Resources (TSX: ARN);

– Argent Energy (TSX: AET);

– Armtec Infrastructure (TSX: ARF) – this patient is being kept alive and bled slowly to death by Brookfield, so the actual time of death may be prolonged;

– Connacher Oil and Gas (TSX: CLL)

– Exall Energy (TSX: EE) – On or around February 13, 2015!

– Ivanhoe Energy (TSX: IE)

… and others.

There is significant opportunity here to pick up players (none of which have been named yet anywhere on this site) which appear to be going down but should be able to weather the storm. When companies with December 31 year-ends have to report audited financial statements by March 31, bank covenants are likely to be breached and the negotiations between now and then will be very unpleasant for all involved.

Even big players like Penn West (TSX: PWT) are publicly talking about covenants.

Speaking of covenants, Pinetree Capital (TSX: PNP) has today (January 23, 2015) to cure a debt-to-assets covenant or face default. If they can’t, then they’ll be forced into insolvency by debtholders on January 26, 2015. This would end one of the saddest, yet fascinating, episodes of capital management.

Not in the same category but I think common holders of Canadian Oilsands may be unpleasantly surprised in the next few months or maybe even next few days. The company has quite a pile of debt and (unhedged) Syncrude breakeven is not going to leave any cash for dividends. They already spoke about a cut to 20 cents/share starting this quarter, but I wonder whether they won’t cut further. Management is prudent…

My guess with COS is they’ll cut to 5 to 10 cents a quarter on their January 29th earnings report. COS is relatively advantaged, however, in that their debt maturity structure is quite accommodating – their next significant debt maturity is in 2019 (US$500M). They can wait it out and will easily survive.

Agreed; I think a further sharp selloff in COS would make it an interesting candidate for further consideration.