One observation: It is abundantly clear that oil and gas producers in North America are going to be trimming their 2015 capital budgets. This will disproportionately affect the service companies, but most of this has already been baked into equity prices.

I have no idea where oil prices will be going in the short term. There is plenty of incentive for those that have already sunk a boatload of costs into their wells to keep them flowing. In the short term you might see some price shocks, but in the medium and long term, I cannot see oil losing too much demand relative to supply levels. While getting into my vehicle and experiencing heavy traffic is hardly a statistical sample that you can extrapolate across the world, intuitively I do not think electrification of transportation is going to be an imminent threat on crude oil (or natural gas) as being the transport fuel of choice. Nor do I see the requirements for plastics or any derivative products of crude being replaced anytime soon.

The point of the preceding paragraph is that crude oil is not going to disappear off the map anytime soon (unlike its predecessor, which was whale oil).

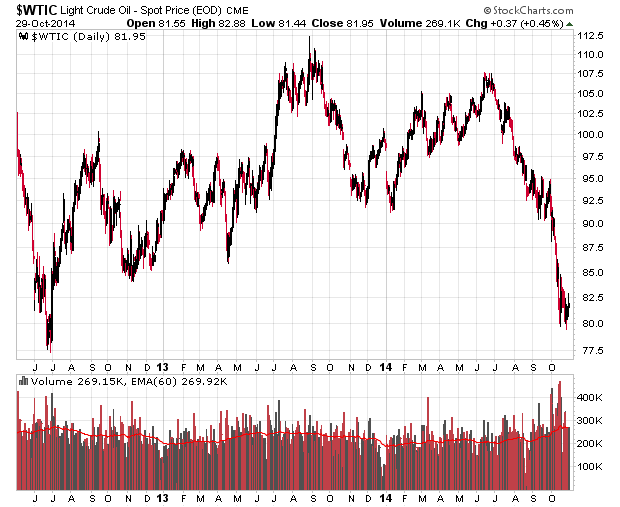

With my very generalized valuation theory on oil and gas producers that “oil prices are a reasonable proxy for company performance plus financial leverage effects”, I note that WTIC (West Texas Intermediate Crude) reached the US$80/barrel level back in June of 2012:

A very simple theory is that oil and gas producers that are trading below what they were trading in June of 2012 should be given a second look to see what caused their relative dis-valuation from present oil levels. A surprisingly large number of Canadian oil and gas companies are trading well above their June 2012 levels despite the oil price difference.

One reason is simply due to good (or lucky timing!) hedging strategies.

Another is due to the mix of oil (and the different types of oil), transport issues, and the percentage of natural gas and natural gas liquids in the revenue mix of a company – in general, while you aren’t suffering pure hell at US$2.50/GJ back in June 2012, your typical gas driller hasn’t been wildly profitable compared to the good ol’ days back in 2008 when you were at US$10.

There’s also the simple reason of having excessive financial leverage and not being able to finance the corporation at revenues obtained at current prices.

There’s plenty of reasons why an oil and gas company would be trading lower today than in even worse price environments seen in June 2012.

So given everything trading on the TSX, I’ve done some homework as a starting point and gone through the companies with the following criteria:

– Share price over CAD$2

– Market cap over $1 billion

– Not a foreign entity (although they can have foreign operations).

– Trading lower today than they generally were in June 2012.

We have, in descending order of market cap:

CVE.TO

TLM.TO (not that they’ve been having difficulties lately!)

BTE.TO

PWT.TO

PGF.TO

TET.TO

BNP.TO

LTS.TO (I was a prolific writer that commented on its ridiculously high valuation when it was known as Petrobakken).

I note that Canadian Oil Sands (COS.TO) is trading barely above what it was in June 2012. This is probably the most purest equity play on WTIC possible beyond putting money in USO (not advisable).

Any thoughts? Comments appreciated.

There is a similar “screen” this morning in the Globe and Mail’s ROB. They too start with market cap of $1B, but rather than focus on share price two years ago verses now, they hone in on the usual metrics for oil companies: ebitda and recycle ratio. Interestingly, BTE is common to both screens. One name that stands out is WCP and is worth a hard look. If you do have nerves of steel per your article yesterday, another name to kick the tires on is DTX. It doesn’t meet the market cap for the screen but has no long term debt, well regarded management, current insider buying from directors, decent hedging program, excellent metrics. My view is that companies with the best balance sheets will gain the most once the oil price funk fades…and it always does.

Avoid: any shale oil producers like LTS. The Bakken play has a good chance of becoming the worlds new swing supply for the reasons you state. The OPEC meeting later this month will be closely watched. The Saudis are flexing their muscles, perhaps testing the level of pain tolerance for the US shale oil industry.

Avoid: any companies already in train wreck mode like Talisman. A perpetual and chronic underperformer. Their latest reporting underscores this.

Avoid: companies with poor balance sheets. I would put Pengrowth and PennWest in this category.

I have no idea either where the price of WTI is headed…but as they say the best cure for a low price is a low price.

Full disclosure: I own WCP, DTX, CVE, ECA, RMP

Thank you for this most interesting comment. You gave me a bit to research.

Another crude metric (get it, crude?) is debt per barrel/day equivalent.

The financial leverage is going to kill some of them, or rather the shareholders, (LTS being a good candidate when they try to renegotiate their credit facility), but I don’t see entities like PGF/PWT getting into solvency trouble (at least yet). e.g., looking at PGF debentures on the TSX, they are still above par value although the company is probably a touch over-leveraged.

I try to imagine if/when the company’s solvency position starts to become an issue with its own operations and in the example of PWT, their facility is good until 2019 which should be a good enough waiting time to have crude prices rise again.

Heavy oil producers I’ve noticed become roadkill first (OPTI being a recent one, CLL being close to death’s door, and STP is probably a heartbeat away). Some light ones are going (ARN, SEQ, etc.) but until we start seeing these marginal guys going away, it will be a tough slog for the majors as well.

Probably my constraint here is having the time go do all the heavy research on these individual firms. Other analysts out there would have probably done the homework and spreadsheeted everything, and this would simply suggest the “home-made ETF” strategy would work best, subtracting the less solvent entities. All of this of course depends on an assumption that WTIC is closer to the bottom than its historical 5-year price history.

Putting the magnifying glass over PWT and PGF for a second, they fall within the poor balance sheet category for me for a few reasons. Perhaps the word to use is “poorer” because I look at them in the context of their peer group which is dividend paying E&Ps. The yield on both these companies has shot up to the 10% level, and the conversation invariably turns to dividend sustainability when the underlying commodity price goes in the crapper. The usual measures for div sustainability are debt to cash flow and total payout ratio. PWT is in the worst shape within their peer group on both these measures, and PGF not far behind. For example, the estimated 2015 payout ratio for both is over 160%. A number below 125% is generally considered reasonable for a healthy balance sheet.

To be clear, I don’t see any imminent dividend cuts coming. All looks good at an $80 WTI average for 2015. At $70, I’m not so sure. More to the point for this conversation is the effect of of a cut on the share price. And once in the penalty box…

It’s not at all that their balance sheets are horrible and will face liquidity issues, it’s how their balance sheets compare to their peers and on that basis I think there are better choices. But alas, those choices haven’t had their share price hammered nearly as much!

Cheers.

The yield is simply a function of market price, but the actual dollars-and-cents as a fraction of the cash they pull in (minus sustaining capital expenditures) is as you pointed out, the more relevant ratio.

PGF is suffering from their heavy oil project that requires a ton of capital up front but once that gets operational in 2015 then their numbers would presumably start looking more realistic and sustainable.

PWT did a half-cut of their dividend in the previous year once the new CEO took control. A good decision even though they knew it would kill their share price, it did give them necessary financial flexibility.

Interesting how CNQ and the rest of them are “full speed ahead” on their capex, but all mention how they are willing to pull the budget on contingent notice.

I like DTX more than WCP, but those ones you cherry-picked obviously are going to survive. The fact that DTX doesn’t give out a dividend is a plus since some market value is ascribed out of those income investors out there that just go for yield, yield and more yield. November 4th, in retrospect, was a great time to buy but haven’t done my DD yet. With the calendar year coming to a close I’d expect that one would be ripe for tax-loss selling, especially since they did their secondary offering at double-digit share prices (sucks to be them…)

TGL is also interesting if you have specific insight on the Egyptian political climate and their crown corporation (specifically their oil company).

There’s going to be a lot of pickings here between now and year end I would suspect.